Issue 4: Funding and Financing

1. Conceptual Foundation

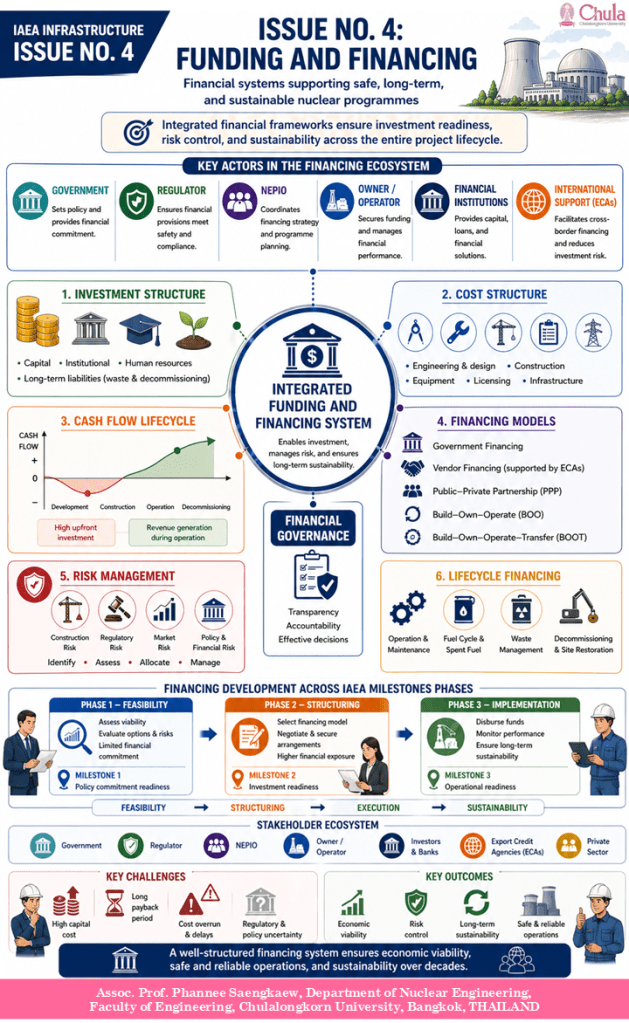

Within the framework of the International Atomic Energy Agency 19 Infrastructure Issues, Issue 4: Financing refers to the establishment of a comprehensive and sustainable financial system that supports all phases of a nuclear power programme. This system must extend beyond the provision of capital for plant construction and encompass the full lifecycle of nuclear activities, including infrastructure development, regulatory oversight, operational management, waste management, and eventual decommissioning.

Nuclear power programmes are characterized by high capital intensity, long construction and operational periods, and stringent safety and regulatory requirements. As a result, financing must be designed not as a short-term investment mechanism but as a long-term institutional framework capable of sustaining the programme over several decades. In this context, financing becomes a strategic enabler that ensures the continuity, safety, and reliability of nuclear energy systems.

2. Definition and Scope

According to guidance from the International Atomic Energy Agency, financing encompasses all mechanisms through which financial resources are mobilized, allocated, and managed to support the nuclear programme. This includes not only the funding of nuclear power plant construction but also the financial support required for regulatory bodies, safety infrastructure, human resource development, and long-term obligations such as radioactive waste management and decommissioning.

The scope of financing therefore extends across both technical and institutional domains. It requires the integration of economic planning with regulatory compliance and safety objectives, ensuring that financial limitations do not compromise the integrity of nuclear safety systems. A well-designed financing structure must balance cost efficiency with risk management and long-term sustainability.

3. Core Components of Nuclear Financing

3.1 Capital Investment and Cost Structure

The development of a nuclear power plant requires substantial upfront capital investment, often representing one of the largest infrastructure expenditures undertaken by a State. This investment includes costs associated with engineering design, procurement of equipment, construction activities, licensing and regulatory compliance, and integration with the national electricity grid.

In addition to these direct costs, financial planning must account for indirect expenditures, including contingency reserves, interest during construction, and risk mitigation provisions. The extended construction period increases financial exposure, as delays can significantly increase total project cost through accumulated interest and contractual penalties. Therefore, cost estimation and financial planning must be conducted with a high degree of accuracy and conservatism.

3.2 Financing Models and Institutional Arrangements

The selection of an appropriate financing model is a critical decision that influences risk allocation, project governance, and long-term financial sustainability. Several financing approaches may be adopted, depending on national policy, market structure, and institutional capacity.

In a state-financed model, the government assumes full responsibility for funding, which provides strong control but also places the financial burden entirely on public resources. In contrast, utility-based models transfer financial responsibility to national utilities, which may operate under regulated or competitive market conditions.

Public–Private Partnership (PPP) models introduce private sector participation, enabling risk sharing between public and private entities. Similarly, vendor financing arrangements, such as Build–Own–Operate (BOO) or Build–Own–Operate–Transfer (BOOT), involve technology suppliers taking on significant financial and operational roles.

Each model presents trade-offs in terms of risk distribution, financing cost, and institutional complexity. Consequently, the chosen model must align with the State’s economic conditions, regulatory framework, and long-term energy strategy.

3.3 Risk Allocation and Financial Risk Management

Nuclear projects are associated with multiple categories of financial risk, including construction risk, regulatory risk, market risk, and political risk. Construction risk arises from potential delays and cost overruns, while regulatory risk relates to uncertainties in licensing and compliance requirements. Market risk is linked to fluctuations in electricity prices, and political risk reflects changes in national policy or public acceptance.

Effective financing requires that these risks be systematically identified, quantified, and allocated among stakeholders. This is typically achieved through contractual arrangements, government guarantees, insurance mechanisms, and international agreements. Proper risk allocation is essential to ensure that no single party bears disproportionate risk, which could otherwise undermine project viability.

3.4 Lifecycle Financing and Long-Term Financial Provisions

A nuclear financing framework must address the entire lifecycle of the facility, extending beyond construction and operation. This includes the management of spent nuclear fuel, radioactive waste disposal, and the eventual decommissioning of the plant.

To ensure that these long-term obligations are met, dedicated financial mechanisms must be established early in the programme. These may include decommissioning funds, waste management funds, and financial assurance instruments. Such provisions must be regularly reviewed and adjusted to reflect changes in cost estimates and operational conditions.

3.5 Institutional and Regulatory Funding

In addition to project-specific financing, adequate funding must be provided for the institutional framework that supports nuclear safety and regulation. Independent regulatory bodies must have sufficient financial resources to perform licensing, inspection, and enforcement functions effectively.

Similarly, funding is required for emergency preparedness systems, technical support organizations, and national infrastructure development. Insufficient financial support in these areas may compromise regulatory independence and weaken the overall safety framework.

4. Progression of Financing Across IAEA Milestones Phases

The development of financing systems follows the three phases of the International Atomic Energy Agency Milestones approach, reflecting increasing levels of financial commitment, institutional capability, and risk exposure.

During Phase 1, financing activities are primarily analytical and strategic in nature. The State evaluates the economic feasibility of nuclear power within its national energy policy framework and conducts preliminary assessments of cost, affordability, and funding options. At this stage, various financing models are explored, and potential risks are identified. Financial commitments remain limited, but the foundation for future investment decisions is established.

The achievement of Milestone 1, defined as readiness to make a knowledgeable commitment to a nuclear power programme, indicates that the State has developed a sufficiently robust understanding of financial requirements, risks, and strategic options.

During Phase 2, financing transitions from conceptual analysis to structured implementation. The State selects an appropriate financing model and begins formal negotiations with investors, technology vendors, and financial institutions. Detailed financial arrangements are established, including contractual frameworks, risk-sharing mechanisms, and funding agreements. Financial exposure increases significantly during this phase, as commitments become binding and project development activities intensify.

The achievement of Milestone 2, defined as readiness to invite bids for the first nuclear power plant, demonstrates that the State has secured viable financing arrangements and established a financial structure capable of supporting project implementation.

During Phase 3, financing systems become fully operational and actively managed. Financial resources are disbursed to support construction, commissioning, and operation of the nuclear power plant. Continuous monitoring of cost, schedule, and financial performance is conducted to ensure alignment with project objectives. In addition, long-term financial provisions for waste management and decommissioning are implemented and maintained. Financial management becomes an integral part of operational governance, ensuring that the programme remains economically sustainable over its lifetime.

The achievement of Milestone 3, defined as readiness to commission and operate the first nuclear power plant, indicates that the financing system is capable of supporting sustained operation and managing long-term financial obligations.

5. Conceptual Interpretation of Financing Development

The progression of financing across the three phases can be conceptualized as a transition from feasibility assessment, to financial structuring, and ultimately to financial execution and long-term sustainability. This evolution highlights that financing is not a static input but a dynamic system that develops alongside the nuclear programme.

6. Key Challenges

Financing nuclear power programmes presents several significant challenges. The high upfront capital requirements and long payback periods can limit access to financing, particularly for newcomer countries. In addition, cost overruns and project delays can substantially increase financial risk.

Regulatory uncertainty and policy changes may also affect investor confidence. Furthermore, balancing economic considerations with safety requirements remains a persistent challenge, as cost pressures must not compromise safety performance.

7. Integrated Perspective

Financing is closely interconnected with other infrastructure issues, including national policy (Issue 1), management systems (Issue 3), legal frameworks (Issue 5), regulatory systems (Issue 7), and human resource development (Issue 10). It serves as an enabling mechanism that allows all components of the nuclear infrastructure to function effectively.

8. Concluding Perspective

Financing is a critical determinant of the success and sustainability of a nuclear power programme. A well-structured financing system ensures that sufficient resources are available at all stages of the programme, while maintaining alignment with safety, regulatory, and operational requirements.

Ultimately, financing must be designed as an integrated, long-term system that supports not only economic viability but also the safe and reliable operation of nuclear energy systems over decades.

Issue No. 4: การเงินและการจัดหาเงินทุน (Funding and Financing)

1. แนวคิดพื้นฐาน

ภายใต้กรอบโครงสร้างพื้นฐาน 19 ด้าน ของทบวงการพลังงานปรมาณูระหว่างประเทศ (International Atomic Energy Agency: IAEA) ประเด็นด้านที่ 4 การเงินและการจัดหาเงินทุน หมายถึง การจัดตั้งระบบทางการเงินที่ครอบคลุมและยั่งยืน ซึ่งสามารถรองรับการดำเนินโครงการพลังงานนิวเคลียร์ในทุกระยะของวัฏจักรการดำเนินโครงการ ตั้งแต่การกำหนดนโยบาย การออกแบบและก่อสร้าง การดำเนินงาน ไปจนถึงการเลิกใช้งานและการจัดการกากกัมมันตรังสี

ในบริบทของโครงการพลังงานนิวเคลียร์ การเงินมิได้จำกัดอยู่เพียงการจัดหาเงินลงทุนสำหรับการก่อสร้างโรงไฟฟ้าเท่านั้น แต่เป็นระบบเชิงโครงสร้างที่ต้องสนับสนุนทั้งมิติทางเทคนิค มิติด้านสถาบัน และมิติด้านความปลอดภัย โดยต้องสามารถรองรับภาระผูกพันระยะยาวที่อาจยาวนานหลายทศวรรษ

ลักษณะเฉพาะของโครงการนิวเคลียร์ ได้แก่ การใช้เงินลงทุนเริ่มต้นสูง ระยะเวลาก่อสร้างยาวนาน และข้อกำหนดด้านความปลอดภัยที่เข้มงวด ส่งผลให้ระบบการเงินต้องถูกออกแบบในลักษณะของระบบระยะยาวที่สามารถบริหารความเสี่ยงและความไม่แน่นอนได้อย่างมีประสิทธิภาพ

2. นิยามและขอบเขต

ตามแนวทางของ IAEA การเงินในบริบทของโครงการพลังงานนิวเคลียร์หมายถึงกระบวนการทั้งหมดในการระดม จัดสรร และบริหารทรัพยากรทางการเงิน เพื่อสนับสนุนกิจกรรมของโครงการอย่างครบถ้วน ขอบเขตดังกล่าวครอบคลุมทั้งการลงทุนในโรงไฟฟ้า การสนับสนุนหน่วยงานกำกับดูแล การพัฒนาทรัพยากรมนุษย์ และการจัดตั้งกองทุนสำหรับภาระผูกพันระยะยาว เช่น การจัดการกากกัมมันตรังสีและการรื้อถอนโรงไฟฟ้า

ระบบการเงินจึงต้องบูรณาการระหว่างเศรษฐศาสตร์ ความปลอดภัย และการกำกับดูแล เพื่อให้มั่นใจว่าข้อจำกัดทางการเงินจะไม่ส่งผลกระทบต่อมาตรฐานความปลอดภัย

3. องค์ประกอบหลักของระบบการเงิน

3.1 การลงทุนและโครงสร้างต้นทุน

การลงทุนในโครงการพลังงานนิวเคลียร์สามารถจำแนกได้เป็นหลายประเภทตามลักษณะของกิจกรรมและช่วงเวลาของโครงการ โดยการลงทุนหลักครอบคลุมค่าใช้จ่ายด้านการออกแบบ &วิศวกรรม การจัดซื้อ และการก่อสร้างโรงไฟฟ้า รวมถึงโครงสร้างพื้นฐานสนับสนุน เช่น ระบบโครงข่ายไฟฟ้า

นอกจากนั้น ยังมีการลงทุนเชิงสถาบัน ซึ่งเกี่ยวข้องกับการจัดตั้งหน่วยงานกำกับดูแล ระบบกฎหมาย และโครงสร้างพื้นฐานด้านความปลอดภัย ตลอดจนการลงทุนด้านทรัพยากรมนุษย์ ซึ่งครอบคลุมการพัฒนาบุคลากรในระยะยาว

ในอีกมิติหนึ่ง การลงทุนสำหรับภาระผูกพันในอนาคต เช่น กองทุนการรื้อถอนและการจัดการกากกัมมันตรังสี ก็มีความสำคัญอย่างยิ่ง และต้องมีการวางแผนตั้งแต่ระยะเริ่มต้น

3.2 กระแสเงินสดตลอดวงจรของโครงการ

ลักษณะของกระแสเงินสดในโครงการพลังงานนิวเคลียร์มีความเฉพาะตัว โดยในช่วงเริ่มต้นของโครงการจะมีการใช้เงินลงทุนจำนวนมากโดยยังไม่มีรายได้เกิดขึ้น ซึ่งเรียกว่าเป็นช่วงของการลงทุนเริ่มต้น เมื่อโครงการเข้าสู่ระยะดำเนินงาน รายได้จากการผลิตไฟฟ้าจะเริ่มเกิดขึ้น อย่างไรก็ตาม รายได้สุทธิจะเกิดขึ้นได้ก็ต่อเมื่อสามารถครอบคลุมต้นทุนทั้งหมด รวมถึงต้นทุนทางการเงินและค่าใช้จ่ายในการดำเนินงาน ลักษณะนี้สะท้อนให้เห็นว่าโครงการนิวเคลียร์ต้องอาศัยความมั่นคงทางการเงินในระยะยาว และมีระยะเวลาคืนทุนที่ยาวนาน

3.3 รูปแบบการจัดหาเงินทุน

รูปแบบการจัดหาเงินทุนสามารถจำแนกได้ตามโครงสร้างความร่วมมือและบทบาทของผู้มีส่วนได้ส่วนเสีย โดยรูปแบบที่สำคัญ ได้แก่

- การจัดหาเงินทุนโดยภาครัฐ (Government Financing) ซึ่งรวมถึงการใช้เงินงบประมาณของรัฐหรือการกู้ยืมในระดับประเทศ (sovereign loans) ซึ่งช่วยลดความเสี่ยงด้านการลงทุน

- การจัดหาเงินทุนโดยผู้จำหน่ายเทคโนโลยี (Vendor Financing) ซึ่งมักเกี่ยวข้องกับหน่วยงานให้สินเชื่อเพื่อการส่งออก (Export Credit Agencies: ECAs)

- ความร่วมมือระหว่างภาครัฐและเอกชน (Public–Private Partnership: PPP) ซึ่งเป็นรูปแบบการแบ่งปันความเสี่ยงระหว่างภาครัฐและภาคเอกชนในช่วงระยะเวลาหนึ่ง

รูปแบบBuild–Own–Operate (BOO) และBuild–Own–Operate–Transfer (BOOT) ซึ่งผู้ลงทุนหรือผู้จำหน่ายเทคโนโลยีมีบทบาทในการเป็นเจ้าของและดำเนินการโรงไฟฟ้า

3.4 การจัดสรรความเสี่ยงและการบริหารความเสี่ยงทางการเงิน

โครงการพลังงานนิวเคลียร์มีความเกี่ยวข้องกับความเสี่ยงทางการเงินหลายประเภท ซึ่งรวมถึงความเสี่ยงด้านการก่อสร้าง ความเสี่ยงด้านการกำกับดูแล ความเสี่ยงด้านตลาด และความเสี่ยงเชิงนโยบายหรือการเมือง

ความเสี่ยงด้านการก่อสร้างเกิดจากความเป็นไปได้ของความล่าช้าในการดำเนินโครงการและการเพิ่มขึ้นของต้นทุนเกินกว่าที่ประมาณการไว้ ขณะที่ความเสี่ยงด้านการกำกับดูแลเกี่ยวข้องกับความไม่แน่นอนของกระบวนการอนุญาต การออกใบอนุญาต และข้อกำหนดด้านการปฏิบัติตามกฎระเบียบ

ในส่วนของความเสี่ยงด้านตลาด มีความเชื่อมโยงกับความผันผวนของราคาพลังงานไฟฟ้าและสภาวะการแข่งขันในตลาดพลังงาน ส่วนความเสี่ยงเชิงนโยบายหรือการเมืองสะท้อนถึงการเปลี่ยนแปลงของนโยบายระดับชาติ ทิศทางการพัฒนาพลังงานของประเทศ หรือระดับการยอมรับของสาธารณชน

การจัดหาเงินทุนที่มีประสิทธิภาพจำเป็นต้องอาศัยการระบุ การประเมินเชิงปริมาณ และการจัดสรรความเสี่ยงเหล่านี้อย่างเป็นระบบระหว่างผู้มีส่วนได้ส่วนเสีย โดยกระบวนการดังกล่าวมักดำเนินการผ่านกลไกต่าง ๆ เช่น การกำหนดเงื่อนไขในสัญญา การค้ำประกันโดยภาครัฐ การใช้เครื่องมือประกันความเสี่ยง และความตกลงระหว่างประเทศ

การจัดสรรความเสี่ยงอย่างเหมาะสมมีความสำคัญอย่างยิ่ง เนื่องจากช่วยป้องกันไม่ให้ภาระความเสี่ยงตกอยู่กับฝ่ายใดฝ่ายหนึ่งมากเกินไป ซึ่งอาจส่งผลกระทบต่อความเป็นไปได้และความยั่งยืนของโครงการในระยะยาว

3.5 ผู้มีส่วนได้ส่วนเสียในระบบการเงิน

ระบบการเงินของโครงการนิวเคลียร์เกี่ยวข้องกับผู้มีส่วนได้ส่วนเสียหลายฝ่าย ได้แก่ ภาครัฐ หน่วยงานกำกับดูแล องค์กรดำเนินโครงการ ผู้ดำเนินการโรงไฟฟ้า นักลงทุน ธนาคาร และหน่วยงานให้สินเชื่อเพื่อการส่งออก ผู้มีส่วนได้ส่วนเสียแต่ละฝ่ายมีบทบาทในการลงทุน การบริหารความเสี่ยง และการกำหนดเงื่อนไขทางการเงิน ซึ่งต้องทำงานร่วมกันอย่างสอดคล้อง

4. พัฒนาการของระบบการเงินตามระยะของ IAEA Milestones

การพัฒนาระบบการเงินดำเนินไปตามสามระยะของกรอบการกำหนดหมุดหมาย (Milestones) ของ IAEA ซึ่งสะท้อนถึงระดับความผูกพันทางการเงิน ขีดความสามารถของสถาบัน และระดับความเสี่ยงที่เพิ่มขึ้นอย่างต่อเนื่อง

ในระยะที่ 1 กิจกรรมด้านการเงินมีลักษณะเชิงวิเคราะห์และเชิงกลยุทธ์เป็นหลัก โดยรัฐจะทำการประเมินความเป็นไปได้ทางเศรษฐกิจของการพัฒนาโครงการพลังงานนิวเคลียร์ภายใต้กรอบนโยบายพลังงานของประเทศ รวมทั้งดำเนินการวิเคราะห์เบื้องต้นเกี่ยวกับต้นทุน ความสามารถในการรองรับภาระทางการเงิน และทางเลือกในการจัดหาเงินทุน ในระยะนี้จะมีการสำรวจรูปแบบการจัดหาเงินทุนที่หลากหลาย และทำการระบุความเสี่ยงที่อาจเกิดขึ้น แม้ว่าการผูกพันทางการเงินจะยังอยู่ในระดับจำกัด แต่ถือเป็นช่วงสำคัญในการวางรากฐานสำหรับการตัดสินใจลงทุนในอนาคต

การบรรลุหมุดหมายที่ 1 ซึ่งหมายถึงความพร้อมในการตัดสินใจเชิงนโยบายอย่างมีข้อมูล (readiness to make a knowledgeable commitment to a nuclear power programme) แสดงให้เห็นว่ารัฐมีความเข้าใจที่เพียงพอเกี่ยวกับความต้องการทางการเงิน ความเสี่ยง และทางเลือกเชิงกลยุทธ์ที่เกี่ยวข้อง

ในระยะที่ 2 ระบบการเงินจะพัฒนาจากการวิเคราะห์เชิงแนวคิดไปสู่การดำเนินการเชิงโครงสร้าง โดยรัฐจะทำการเลือกรูปแบบการจัดหาเงินทุนที่เหมาะสม และเริ่มกระบวนการเจรจาอย่างเป็นทางการกับนักลงทุน ผู้จำหน่ายเทคโนโลยี และสถาบันการเงิน มีการจัดทำโครงสร้างทางการเงินอย่างละเอียด ซึ่งรวมถึงกรอบสัญญา กลไกการแบ่งปันความเสี่ยง และข้อตกลงด้านเงินทุน

ในระยะนี้ ระดับความเสี่ยงทางการเงินจะเพิ่มสูงขึ้นอย่างมีนัยสำคัญ เนื่องจากการผูกพันทางการเงินเริ่มมีผลผูกพันทางกฎหมาย และกิจกรรมการพัฒนาโครงการมีความเข้มข้นมากขึ้น

การบรรลุหมุดหมายที่ 2 ซึ่งหมายถึงความพร้อมในการเชิญชวนเสนอราคาเพื่อก่อสร้างโรงไฟฟ้านิวเคลียร์เครื่องแรก (readiness to invite bids for the first nuclear power plant) แสดงให้เห็นว่ารัฐได้จัดเตรียมโครงสร้างทางการเงินที่มีความเป็นไปได้ และสามารถรองรับการดำเนินโครงการได้อย่างเป็นรูปธรรม

ในระยะที่ 3 ระบบการเงินจะเข้าสู่การดำเนินงานอย่างเต็มรูปแบบ โดยมีการบริหารจัดการทางการเงินอย่างต่อเนื่องและเป็นระบบ ทรัพยากรทางการเงินจะถูกจัดสรรเพื่อสนับสนุนการก่อสร้าง การทดสอบเดินเครื่อง และการดำเนินงานของโรงไฟฟ้านิวเคลียร์

ในระยะนี้ จะมีการติดตามและควบคุมต้นทุน ระยะเวลา และประสิทธิภาพทางการเงินอย่างต่อเนื่อง เพื่อให้สอดคล้องกับเป้าหมายของโครงการ ขณะเดียวกัน จะมีการจัดตั้งและบริหารกองทุนระยะยาวสำหรับการจัดการกากกัมมันตรังสีและการรื้อถอนโรงไฟฟ้าอย่างเป็นระบบ

การบริหารจัดการทางการเงินในระยะนี้จะกลายเป็นส่วนหนึ่งของระบบธรรมาภิบาลขององค์กร โดยมีบทบาทสำคัญในการรักษาความมั่นคงทางเศรษฐกิจของโครงการตลอดอายุการใช้งาน

การบรรลุหมุดหมายที่ 3 ซึ่งหมายถึงความพร้อมในการเดินเครื่องและดำเนินงานโรงไฟฟ้านิวเคลียร์เครื่องแรก (readiness to commission and operate the first nuclear power plant) แสดงให้เห็นว่าระบบการเงินมีความสามารถในการสนับสนุนการดำเนินงานในระยะยาว และสามารถบริหารภาระผูกพันทางการเงินได้อย่างยั่งยืน

5. มุมมองเชิงแนวคิด

พัฒนาการของระบบการเงินสามารถตีความได้ว่าเป็นการเปลี่ยนผ่านเชิงระบบจากระยะของการวิเคราะห์ความเป็นไปได้และการประเมินความเสี่ยง ไปสู่ระยะของการจัดโครงสร้างทางการเงินและการกำหนดกลไกการลงทุน และท้ายที่สุดพัฒนาไปสู่ระยะของการดำเนินงานจริง ซึ่งต้องอาศัยการบริหารจัดการทางการเงินอย่างต่อเนื่อง เพื่อรองรับความยั่งยืนของโครงการในระยะยาว

6. ความท้าทายสำคัญ

การจัดหาเงินทุนสำหรับโครงการพลังงานนิวเคลียร์ต้องเผชิญกับความท้าทายที่สำคัญหลายประการ โดยเฉพาะอย่างยิ่งความต้องการเงินลงทุนเริ่มต้นในระดับสูง และระยะเวลาคืนทุนที่ยาวนาน ซึ่งอาจจำกัดความสามารถในการเข้าถึงแหล่งเงินทุน โดยเฉพาะในประเทศที่เพิ่งเริ่มพัฒนาโครงการพลังงานนิวเคลียร์

นอกจากนี้ ปัญหาต้นทุนบานปลายและความล่าช้าในการดำเนินโครงการสามารถเพิ่มความเสี่ยงทางการเงินได้อย่างมีนัยสำคัญ ซึ่งส่งผลกระทบต่อความเชื่อมั่นของนักลงทุนและความเป็นไปได้ของโครงการ

ความไม่แน่นอนด้านกฎระเบียบและการเปลี่ยนแปลงเชิงนโยบายยังเป็นปัจจัยสำคัญที่อาจส่งผลต่อความเชื่อมั่นของนักลงทุนในระยะยาว ขณะเดียวกัน การสร้างสมดุลระหว่างความคุ้มค่าทางเศรษฐกิจกับข้อกำหนดด้านความปลอดภัยยังคงเป็นความท้าทายที่ต้องได้รับการบริหารจัดการอย่างต่อเนื่อง เนื่องจากแรงกดดันด้านต้นทุนไม่ควรส่งผลกระทบต่อประสิทธิภาพด้านความปลอดภัยของระบบ

7. มุมมองเชิงบูรณาการ

ระบบการเงินมีความเชื่อมโยงอย่างใกล้ชิดกับประเด็นโครงสร้างพื้นฐานด้านอื่นของโครงการพลังงานนิวเคลียร์ ซึ่งรวมถึงนโยบายระดับชาติ (Issue 1) ระบบการบริหารจัดการ (Issue 3) กรอบกฎหมาย (Issue 5) ระบบกำกับดูแล (Issue 7) และการพัฒนาทรัพยากรมนุษย์ (Issue 10)

ในมุมมองเชิงระบบ การเงินทำหน้าที่เป็นกลไกสนับสนุนที่สำคัญ ซึ่งช่วยให้ทุกองค์ประกอบของโครงสร้างพื้นฐานนิวเคลียร์สามารถดำเนินงานได้อย่างมีประสิทธิภาพและสอดคล้องกัน

8. บทสรุป

การเงินและการจัดหาเงินทุนถือเป็นกลไกกำหนดความสำเร็จเชิงระบบของโครงการพลังงานนิวเคลียร์ โดยระบบการเงินที่ได้รับการออกแบบอย่างมีโครงสร้างจะต้องสามารถจัดสรรทรัพยากรทางการเงินได้อย่างเพียงพอในทุกระยะของวัฏจักรการดำเนินโครงการ พร้อมทั้งรักษาความสอดคล้องกับข้อกำหนดด้านความปลอดภัย การกำกับดูแล และการดำเนินงาน

ในระยะยาว ระบบการเงินจำเป็นต้องถูกพัฒนาให้เป็นระบบบูรณาการที่มีความยืดหยุ่นและมีเสถียรภาพ เพื่อรองรับทั้งความคุ้มค่าทางเศรษฐศาสตร์และการดำเนินงานที่ปลอดภัยและเชื่อถือได้ของระบบพลังงานนิวเคลียร์อย่างต่อเนื่อง

References

- International Atomic Energy Agency. (2024).Milestones in the development of a national infrastructure for nuclear power (Rev. 2). Vienna: IAEA.

👉 (NG-G-3.1 Rev.2 — core reference ของ Issue 1–19) - International Atomic Energy Agency. (2022).Financing of new nuclear power plants. Vienna: IAEA.

- International Atomic Energy Agency. (2017).Financing nuclear power plants. Vienna: IAEA Nuclear Energy Series.

- International Atomic Energy Agency. (2014).Economic evaluation of nuclear power plants. Vienna: IAEA.

- Organisation for Economic Co-operation and Development Nuclear Energy Agency. (2020). Unlocking reducing the cost of nuclear: A practical guide for stakeholders. Paris: OECD Publishing.

- World Nuclear Association. (2023). Financing nuclear energy.

ใส่ความเห็น